In the evolving landscape of personal finance, understanding the true cost of your investment platform is paramount. Acorns, a pioneer in micro-investing, has garnered significant attention for its simplified approach, but its unique Acorns fees and pricing structure—a flat monthly subscription—is a critical factor in determining if it's the right fit for your financial journey. While initially appealing for its "spare change" investing model, this fixed monthly cost can have a surprisingly disproportionate impact on your returns, especially as your account balance fluctuates.

Let's dive deep into what you actually pay, what you get for it, and most importantly, whether Acorns offers genuine value for your specific financial situation.

At a Glance: Acorns Fees & Pricing

- Structure: Flat monthly subscription, not based on a percentage of assets.

- Tiers: Bronze ($3/month), Silver ($6/month), Gold ($12/month).

- What You Get: Bundled services including investing, retirement accounts, checking, savings, and (in higher tiers) custodial accounts for kids.

- Hidden Costs: ETF expense ratios (charged by fund providers, not Acorns) and a transfer-out fee ($50 per ETF) if you move your investments elsewhere.

- Key Consideration: The flat fee can represent a high percentage of small account balances, significantly impacting early growth.

Acorns' Core Philosophy: Simplify and Bundle

Acorns was built on the premise of making investing accessible to everyone, regardless of their starting capital or financial expertise. Their flagship "Round-Ups" feature, which automatically invests your spare change from everyday purchases, epitomizes this mission. But Acorns has grown beyond just micro-investing. It now offers a comprehensive suite of financial tools—from diversified investment portfolios and IRAs to banking and custodial accounts—all managed through a slick mobile app.

The core idea is convenience: one platform for investing, saving, and banking, designed to encourage consistent wealth building without requiring active management or complex decisions. This integrated approach, however, comes with a subscription cost that bundles these services together. Understanding this value proposition is key to evaluating its fees.

Breaking Down Acorns' Flat Monthly Subscription Tiers

Unlike many traditional brokerages or even other robo-advisors that charge a percentage of your assets under management (AUM), Acorns operates on a flat monthly fee. This structure means your monthly cost remains the same whether you have $100 or $100,000 in your accounts. While this can be a huge benefit for larger portfolios, it's a significant consideration for those just starting out.

Acorns currently offers three primary subscription tiers, each unlocking more features and benefits:

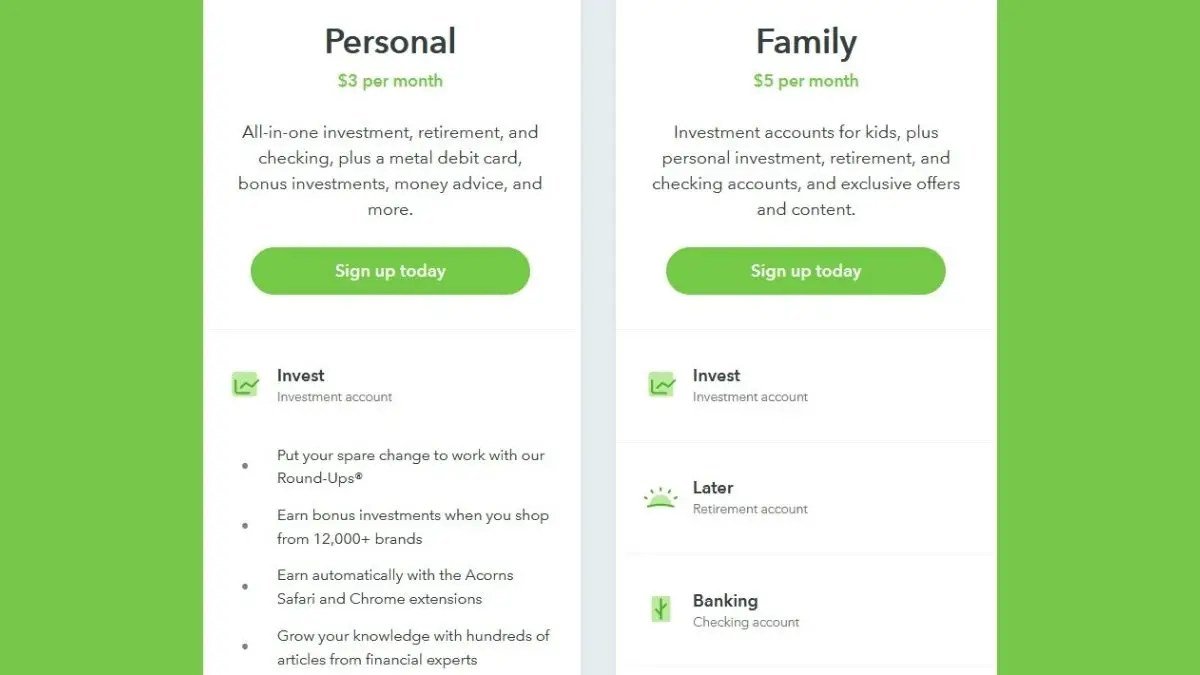

1. Bronze: Your Starting Point ($3/month)

At $3 per month, the Bronze tier (also called "Personal") provides the foundational Acorns experience.

What You Get:

- Acorns Invest: Automated, diversified portfolios built with low-cost ETFs. Acorns handles the rebalancing and fund selection based on your risk tolerance. This is where your Round-Ups and direct deposits go.

- Acorns Later: Access to Individual Retirement Accounts (IRAs) – Traditional, Roth, or SEP – with expert-built portfolios designed for long-term growth.

- Acorns Checking: An online banking account designed to help you save and invest automatically. It includes a heavy metal Acorns Visa™ debit card, no overdraft fees, mobile check deposit, digital checks, and access to 55,000+ fee-free ATMs (AllPoint network).

Who It's For: The Bronze tier is ideal for absolute beginners eager to start investing and saving with minimal effort. If you're looking for a simple, automated way to get your feet wet in investing, contribute to retirement, and manage basic banking, this tier covers the essentials. It's particularly attractive for those who struggle with traditional saving methods and appreciate the Round-Ups feature as a "set it and forget it" tool.

2. Silver: Enhanced Savings & Rewards ($6/month)

Stepping up to the Silver tier (formerly "Personal Plus") doubles your monthly fee but adds several features aimed at boosting your savings and providing more value.

What You Get (All Bronze features, plus):

- Emergency Savings: A dedicated savings account designed to help you build a financial cushion, currently offering a competitive APY (e.g., 3.35% APY, subject to change).

- Acorns Later Match: Acorns will match 1% of your new contributions to your IRA during your first year. This is a direct incentive to save for retirement.

- Enhanced Earning: Bonus investments matched by Acorns, up to 25%, when you shop with partner brands through Acorns Earn.

- Live Q&As: Access to live question-and-answer sessions with investing experts, adding an educational component.

Who It's For: The Silver tier is a good fit for individuals who are serious about building an emergency fund alongside their investments and want a little extra incentive to contribute to their IRA. The enhanced earning opportunities and expert Q&As add value for those looking to accelerate their financial growth and knowledge. If you're past the very beginner stage and want to optimize your savings further, this tier offers compelling features.

3. Gold: Family, Customization & Premium Perks ($12/month)

The Gold tier (formerly "Premium") is Acorns' most comprehensive offering, designed for individuals and families looking for a full suite of financial tools, including accounts for children and advanced planning features.

What You Get (All Silver features, plus):

- Acorns Later Match (Increased): A significant bump to a 3% IRA match on new contributions during your first year (up to a maximum investment from Acorns, e.g., $225 if you max out your annual contribution). This can be a powerful incentive for retirement saving.

- Acorns Early Invest: Automated investment accounts for kids (custodial accounts). This allows you to invest for your children's future with diversified portfolios, also with a 1% match on contributions.

- Custom Portfolios: For those who want more control, this tier allows you to add individual stocks and ETFs to your diversified portfolio, moving beyond the fully automated approach.

- Money Manager (New): A tool that smartly splits your money across investing, saving, and spending, helping you stay on track with financial goals and personalized milestones.

- Acorns Early Money App & Debit Card: A smart money app for kids/teens with parental controls, a chores tracker, automated allowance, and educational videos/quizzes, complemented by a debit card with 35+ designs.

- Exclusive Gold Benefits: A $10,000 life insurance policy (for eligible customers) and a no-cost Will (valued at $259), adding significant value beyond just investments.

- Maximum Earning: Bonus investments matched by Acorns, up to 50%, for shopping with partners.

Who It's For: The Gold tier is best suited for families or individuals with higher income who want an all-in-one financial hub. If you're planning for your children's financial future, want to boost your IRA contributions significantly, appreciate life insurance and estate planning tools, and desire a degree of customization in your portfolio, the $12/month fee can be very competitive compared to managing these services separately. It aggregates value that would otherwise cost more across different providers.

Beyond the Subscription: Other Potential Costs to Consider

While Acorns prides itself on no "hidden fees" or trading commissions, there are a couple of other cost factors that savvy investors should be aware of:

- ETF Expense Ratios: When you invest with Acorns, your money goes into portfolios built from low-cost Exchange Traded Funds (ETFs). These underlying funds have their own small annual fees, known as expense ratios (typically ranging from 0.04% to 0.22%). These aren't charged by Acorns directly but are deducted from the fund's assets by the fund provider. They are a standard part of investing in ETFs, regardless of the brokerage.

- Transfer-out Fees: Should you decide to move your investments from Acorns to another brokerage account, Acorns charges a $50 fee per ETF transferred. This can quickly add up if your portfolio holds multiple different ETFs. It's an important consideration for long-term flexibility.

The "Flat Fee" Dilemma: When Acorns Gets Expensive (or Cheap)

This is perhaps the most critical aspect of Acorns' pricing model. A flat monthly fee can be a double-edged sword.

The High-Cost Scenario: Small Account Balances

When your account balance is small, a flat monthly fee can translate to a surprisingly high percentage of your assets. Let's look at some examples:

- $100 Account (Bronze tier): $3/month means $36 annually. That's a whopping 36% of your balance!

- $500 Account (Bronze tier): $3/month means $36 annually. This is still 7.2% of your balance.

- $1,000 Account (Bronze tier): $3/month means $36 annually. This represents 3.6% of your balance.

In these scenarios, a significant portion of your potential investment returns is eaten up by fees, especially in the early stages when compounding is most crucial. For very small balances, this can make it difficult to see meaningful growth. This is a common criticism, and it's where Acorns' fees can be disproportionately high.

The Low-Cost Scenario: Growing Account Balances

As your account balance grows, the flat fee becomes increasingly cost-effective in percentage terms. - $5,000 Account (Bronze tier): $3/month ($36/year) is just 0.72% of your balance.

- $10,000 Account (Bronze tier): $3/month ($36/year) is a mere 0.36% of your balance.

- $50,000 Account (Gold tier): Even at $12/month ($144/year), this is only 0.29% of your balance.

Compared to robo-advisors that charge 0.25% to 0.50% of AUM, Acorns' flat fee becomes highly competitive, and even cheaper, once your portfolio reaches a certain size, especially for the higher tiers with bundled services. For example, if you have $10,000 invested, a 0.25% AUM fee would be $25 annually. At the $3/month Bronze tier, you'd pay $36 annually, which is slightly more. However, at $50,000, a 0.25% AUM fee is $125 annually, while the Gold tier's $144 annually gives you a plethora of additional banking, retirement, and family-focused benefits.

This means you need to consider not just your current balance, but your projected growth and how much you value the bundled services offered at each tier.

Comparing Acorns: How Its Fees Stack Up

When evaluating Acorns, it’s helpful to benchmark its fees against other options:

- Traditional Brokerages: Many offer commission-free stock and ETF trades, meaning you pay nothing directly to trade. However, they generally don't offer automated portfolio management or bundled banking features. You're on your own to build and manage your portfolio.

- Other Robo-Advisors: Most popular robo-advisors (like Betterment or Wealthfront) typically charge an advisory fee ranging from 0.25% to 0.50% of your assets under management (AUM) annually. This percentage fee model generally scales better for smaller accounts but can become more expensive for very large accounts. They often include services like tax-loss harvesting, which Acorns does not offer.

- Hybrid Advisors: Some services offer human financial advisors for a higher AUM fee (often 0.8% to 1.5% or more) or a flat annual retainer. Acorns does not offer human financial advisors.

Acorns' flat fee truly stands out. It's not a direct apples-to-apples comparison because Acorns bundles so many services. You're paying for convenience, automation, and a suite of financial tools, not just investment management. To truly assess if Acorns is worth it, you need to weigh the value of these integrated services against the pure investment management fee of competitors.

Pros of Acorns' Pricing Model (and the Value You Get)

Despite the upfront cost for small balances, there are significant advantages to Acorns' flat-fee structure and bundled services:

- Predictable Cost: You know exactly what you'll pay each month, simplifying budgeting.

- Motivation for Growth: The flat fee incentivizes you to grow your account. The larger your balance, the smaller the fee becomes as a percentage of your assets.

- Bundled Convenience: Acorns offers investing, banking, retirement, and even accounts for kids all under one roof. Managing these separately could involve multiple apps, passwords, and potentially higher cumulative fees.

- Accessibility: With no minimum to open an account and investments starting at just $5, Acorns makes investing incredibly easy to begin. The Round-Ups feature automates saving for those who struggle to manually set money aside.

- Value at Scale: For larger balances, especially in the Silver and Gold tiers, the flat fee can be significantly cheaper than AUM-based alternatives, especially when considering the added benefits like IRA matches, life insurance, and custom portfolios.

- No Trading Commissions: You won't pay per trade within your Acorns portfolio, which is standard for most modern platforms but still a 'pro'.

Cons and Potential Pitfalls of Acorns' Fees

It's equally important to acknowledge where Acorns' pricing might not be the best fit:

- High Percentage for Small Balances: As discussed, this is the primary drawback. Beginners with very little to invest initially might find the fees eating too much into their returns.

- No Tax-Loss Harvesting: A common feature among many competing robo-advisors, tax-loss harvesting helps optimize tax efficiency by selling investments at a loss to offset capital gains. Acorns does not offer this, which could be a missed opportunity for tax-conscious investors.

- Limited Customization (unless Gold tier): For those who want to pick specific ETFs or have more control over their portfolio beyond general risk tolerance, Acorns' basic tiers offer limited flexibility. The Gold tier introduces some customization, but it comes at a higher price.

- Transfer-out Fees: The $50 per ETF transfer fee can be a deterrent if you decide to move your assets elsewhere later on.

- No Human Financial Advisors: If you prefer direct, personalized advice from a Certified Financial Planner (CFP), Acorns won't provide that service.

Who Acorns' Fee Structure Is Best For

Given its unique fee model and comprehensive features, Acorns generally best suits specific types of investors:

- Beginner Investors: Those new to investing who need a simple, automated, and hands-off approach. The low barrier to entry and Round-Ups are great for building habits.

- Passive Investors: Individuals who prefer not to manage their portfolios actively and trust Acorns' expert-built ETF portfolios and automatic rebalancing.

- Mobile-First Users: Anyone who prefers to manage their finances entirely through a user-friendly mobile app.

- Long-Term Savers: People focused on retirement (Acorns Later) or saving for their children's future (Acorns Early in Gold tier) will find value in the integrated accounts.

- Bundled Service Enthusiasts: If you value having investing, banking, and retirement accounts all integrated into one platform, the convenience and potential cost savings (for larger balances) are appealing.

- Investors with Growing Balances: As your portfolio crosses the $5,000 to $10,000 mark and beyond, the flat monthly fee becomes increasingly competitive compared to AUM-based fees, especially in the Gold tier where the extra benefits truly shine.

Conversely, Acorns might not be the best fit for: - Cost-Sensitive Investors with Very Small Balances: If you only have a few hundred dollars to invest and don't anticipate rapid growth, the flat fee will significantly eat into your returns.

- Active Traders: Acorns is not designed for frequent buying and selling of individual stocks.

- Investors Needing Advanced Tax Strategies: The lack of tax-loss harvesting might be a dealbreaker for some.

- Those Seeking Deep Portfolio Customization: Unless you opt for the Gold tier, portfolio options are limited to Acorns' pre-built models.

Making the Decision: Is Acorns Right for Your Wallet?

Deciding whether Acorns' flat monthly fees are right for you comes down to a few key questions:

- What is your current investment balance, and how quickly do you expect it to grow? If your balance is low ($1,000 or less) and you don't plan to contribute much regularly, the flat fee might be too high in percentage terms. However, if you're consistently contributing and expect your balance to grow, the fee becomes more palatable over time.

- How much do you value convenience and automation? Acorns truly excels at making financial management effortless. If you struggle with saving or investing manually, the set-it-and-forget-it nature could be invaluable.

- Do you need the bundled services? Consider if you would use Acorns Checking, Acorns Later (IRA), Acorns Early (kids' accounts), or the emergency savings. If you would pay for these services separately elsewhere, the bundled fee might offer superior value. For instance, the IRA match in Silver and Gold tiers can quickly offset the monthly cost.

- Are you looking for long-term growth or short-term gains? Acorns is built for long-term investing. Its diversified portfolios and automated rebalancing are designed for patient wealth building, not quick wins.

- Are the "bonus" features worth it to you? The higher tiers offer benefits like life insurance, a free Will, and custom portfolios. Calculate if the value of these perks outweighs the increased monthly fee. For example, getting a free Will and life insurance in the Gold tier might make the $12/month fee a bargain compared to purchasing those services separately.

While the flat monthly fee can seem steep for small balances, Acorns offers a comprehensive financial ecosystem. For those who embrace its automated, bundled approach and commit to consistent contributions, the value proposition, particularly in the higher tiers, can be quite compelling. Ultimately, the "right" choice depends on your personal financial situation, goals, and how you weigh the cost against the convenience and integrated benefits.